Public exchange API

Crypto currencies are bought and sold on different exchanges. Basically it is like a bank, but for crypto. The price at which a token is traded depends on the offer and on the demand. Thus it evolves permanently, every couples of seconds.

It is possible to recover this price using the public API of exchanges. Let’s say you want to know the Bitcoin price in the Kraken exchange. You can do that in your browser, typing this URL:

https://api.kraken.com/0/public/Ticker?pair=BTCEUR

It gives you several information, three being of interest:

last: the price at the last transactionbid: price at which you can sell your cryptoask: price at which you can buy a crypto

Do it programming

It is totally possible to do the same programming. This is handy since it will allow to recover the prices every couple of second automatically.

Here is an example using the R programming language to get the price of the bitcoin on Kraken and showing it in a clean table:

# package

library(tidyverse)

# Recover the information

library(RCurl)

adress <- "https://api.kraken.com/0/public/Ticker?pair=BTCEUR"

ticker <- getURLContent(adress)

# Make the format more readable

require(jsonlite)

tmp <- fromJSON(ticker)$result[[1]]

result <- data.frame(ask=tmp$a[1], bid=tmp$b[1], last=tmp$c[1], open=tmp$o, low=tmp$l[1], high=tmp$h[1], volume=tmp$v[1], volumeQuote=NA, timestamp=NA)

# Show result| ask | bid | last | open | low | high | volume |

|---|---|---|---|---|---|---|

| 5697 | 5697 | 5697 | 5686 | 5671 | 5702 | 56 |

Code resource

I’ve written a set of functions allowing to get the price of many different currencies for the 5 main exchanges. You can easily use these functions. For instance, type the code below in R:

# Source functions that are stored on github

source("https://raw.githubusercontent.com/holtzy/Crypto-Arbitrage/master/FUNCTIONS/Public_Market_Functions.R")

# Use it: price of the bitcoin on bitstamp

get_bitstamp(Sys.time(), "BTCEUR")Harvesting (a lot of) data

I’ve harvested crypto prices:

- for 2 weeks - between the

5th and the 19th of February. - for 5 currencies - bitcoin (BTC), bitcoin cash (BCH), etherum (ETH), litecoin (LTC) and ripple (XRP)

- for 5 exchanges - Coinbase, Kraken, Bitstamp, Bitfinex and Cex.io

This was easily done using an infinite loop that called the functions described above. The exact script used for this work is available here. 800,000 data points were recovered.

The resulting dataset is available on github in a compressed format. You can easily read it in R doing:

# Load the data

load(url("https://raw.githubusercontent.com/holtzy/Crypto-Arbitrage/master/DATA/public_ticker_harvest.Rdata"))

# Have a look to the first lines

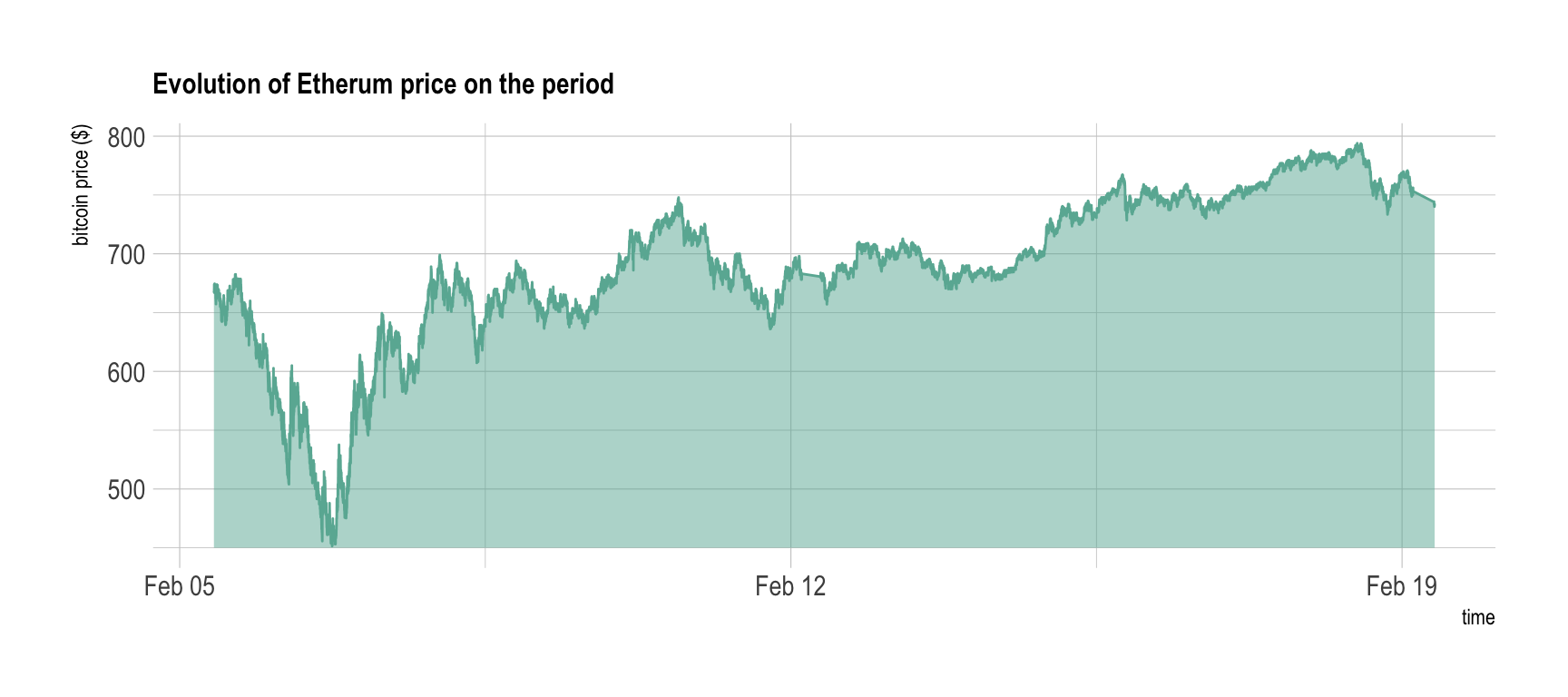

head(Ticker)As a teaser, here is the evolution of the etherum price on Bitstamp on this period of time:

# Load the data

load(url("https://raw.githubusercontent.com/holtzy/Crypto-Arbitrage/master/DATA/public_ticker_harvest.Rdata"))

# Make the plot

library(hrbrthemes)

Ticker %>%

filter( symbol == "ETHEUR" ) %>%

filter(platform == "Bitstamp") %>%

ggplot( aes(x=time, y=as.numeric(last))) +

geom_ribbon(aes(ymin=450, ymax=as.numeric(last)), fill="#69b3a2", color="transparent", alpha=0.5) +

geom_line(color="#69b3a2") +

ggtitle("Evolution of Etherum price on the period") +

ylab("bitcoin price ($)") +

theme_ipsum() +

theme(

plot.title = element_text(size=12)

)

Next step

The next step take this dataset and quantifies the differences between platform. If differences are big enough, we have a chance to perform arbitrage.

A work by Yan Holtz for data-to-viz.com